What is the Precision Gearbox Market and why is it significant?

The Precision Gearbox Market refers to the global industry that designs, manufactures, and supplies high‑accuracy gearboxes used in applications requiring minimal backlash, high torque density, and reliable performance under demanding conditions. Its scope includes planetary, right‑angle, parallel‑shaft, and specialized gearboxes across sectors such as aerospace, robotics, medical devices, and industrial automation. The market is significant because precision gearboxes enable the miniaturization of equipment, improve energy efficiency, and are critical for the performance and safety of advanced machinery.

What are the main drivers, restraints, challenges, and opportunities shaping the Precision Gearbox Market?

Key drivers include rising automation, growth in aerospace and defense programs, and increasing demand for high‑speed robotics and medical instrumentation. Opportunities arise from emerging technologies such as electric‑propulsion aircraft and collaborative robots that require compact, high‑precision power transmission. Restraints involve high manufacturing costs and stringent quality standards that limit entry for new players. Challenges include supply‑chain disruptions for specialty materials and the need for continuous innovation to meet tighter efficiency regulations.

Which growth trends are currently influencing the Precision Gearbox Market?

Current trends feature the shift toward miniaturized gearboxes for portable medical devices, the adoption of additive manufacturing for rapid prototyping of complex gear geometries, and a growing preference for modular gearbox solutions that simplify integration. Additionally, the market is seeing increased use of advanced surface‑coating technologies to enhance wear resistance, and a rise in digital twin simulations that optimize design before physical production.

How did COVID‑19 affect the Precision Gearbox Market and what is the recovery outlook?

The pandemic caused temporary factory shutdowns and delayed aerospace and defense projects, resulting in a short‑term dip in orders. However, the market rebounded quickly as demand for automation and robotics surged to offset labor shortages. Recovery has been reinforced by stimulus spending on infrastructure and medical equipment, positioning the market on a strong growth trajectory that aligns with pre‑COVID plans.

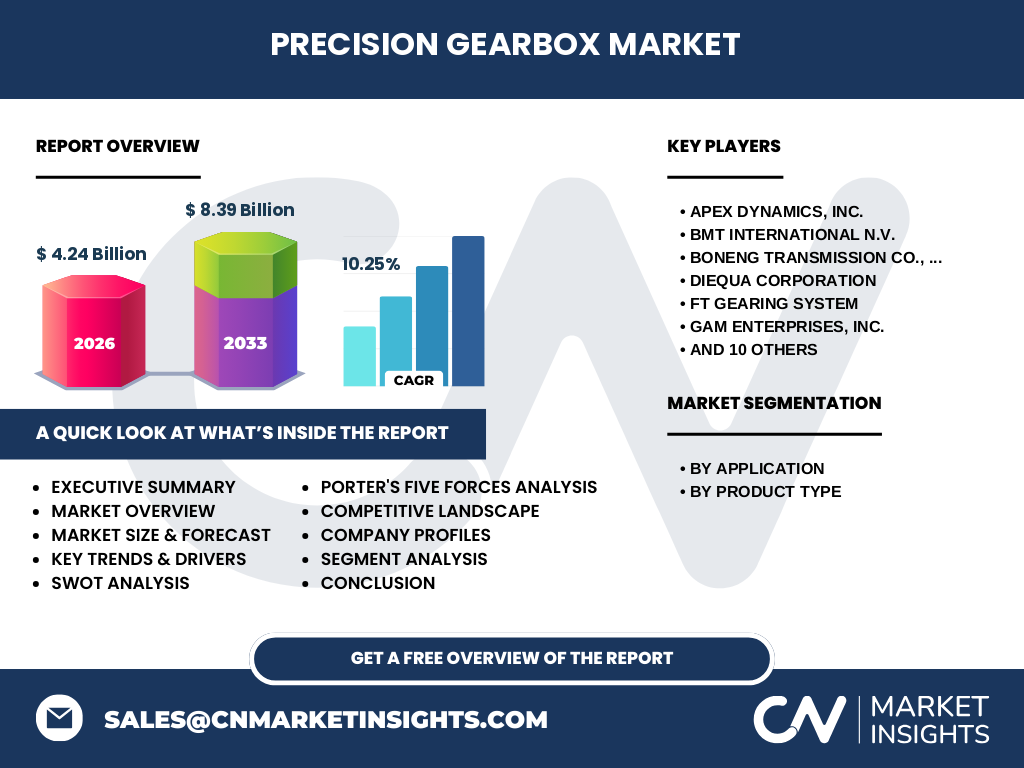

Who are the major competitors and what is the level of consolidation in the Precision Gearbox Market?

Leading competitors include Apex Dynamics, Inc., BMT INTERNATIONAL N.V., Boneng Transmission Co., Ltd., DieQua Corporation, FT Gearing System, GAM Enterprises, Inc., GÔøΩdel Group AG, HIWIN Corporation, Harmonic Drive Systems Inc., Nabtesco Corp, Neugart GmbH, Nidec Corporation, SEW‑EURODRIVE GmbH & Co KG, STBER Antriebstechnik GmbH + Co. KG, Sumitomo Corporation, and WITTENSTEIN SE. The market exhibits moderate consolidation, with several firms pursuing strategic acquisitions and joint ventures to broaden product portfolios and geographic reach.

What are the key findings presented in the Executive Summary of the Precision Gearbox Market report?

The Executive Summary highlights a market valued at $4.24 billion in 2026, projected to reach $8.39 billion by 2033, delivering a CAGR of 10.25 % over the forecast period. Growth is driven by expanding aerospace and robotics sectors, while product innovation and regional demand in Asia‑Pacific are pivotal. Competitive analysis underscores a fragmented landscape with leading players focusing on technology integration and supply‑chain resilience.

What are the forecast expectations for the Precision Gearbox Market from 2025 to 2032?

Based on the provided data, the market is expected to more than double its 2026 value, attaining $8.39 billion by 2033. The consistent 10.25 % CAGR suggests steady expansion each year, supported by rising adoption of precision gearboxes in high‑tech industries and continued investment in R&D across product types.

How is the Precision Gearbox Market sized and shared across its application and product type segments?

Segmented by application, the market serves Military & Aerospace, Food & Beverages, Machine Tools, Material Handling, Packaging Machines, Robotics, Medical Devices, and Others. By product type, it includes Planetary Gearboxes, Right Angle, Parallel Shaft, and Others. While exact monetary splits are not disclosed, all segments collectively contribute to the $4.24 billion base, with high‑growth areas such as Robotics and Medical Devices expected to command a larger share of future sales.

What is the geographic distribution of the Precision Gearbox Market?

The market’s geographic footprint spans North America, Europe, Asia‑Pacific, and Rest of the World. Each region participates in the overall $4.24 billion valuation, with Asia‑Pacific emerging as a strong growth engine due to expanding manufacturing hubs and defense spending, while Europe remains a hub for advanced aerospace applications.

Can you provide a detailed regional analysis of the Precision Gearbox Market?

In North America, growth is driven by defense contracts and automation in automotive manufacturing. Europe benefits from a mature aerospace sector and stringent quality standards that fuel demand for high‑precision solutions. Asia‑Pacific leads in volume production, with rapid industrialization, increasing robotics adoption, and government initiatives supporting advanced manufacturing. The Rest of the World shows modest growth, primarily in emerging economies investing in infrastructure.

What are the profiles and strategic approaches of leading companies in the Precision Gearbox Market?

Companies such as Nidec Corporation and Harmonic Drive Systems focus on R&D and integration of smart sensors into gearboxes. Apex Dynamics emphasizes lightweight designs for aerospace, while SEW‑EURODRIVE leverages its global service network to capture market share in industrial automation. Many firms are expanding through acquisitions—e.g., WITTENSTEIN SE’s recent purchase of a specialized planetary gearbox developer—to broaden technical capabilities.

How does Porter’s Five Forces framework apply to the Precision Gearbox Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is relatively high because specialty steel and heat‑treatment services are limited. Bargaining power of buyers varies; large OEMs negotiate strongly, while niche users have less influence. Threat of substitutes is low, as few alternatives match the precision and durability of gearboxes. Competitive rivalry is intense, with numerous established players competing on technology, reliability, and after‑sales support.

What are the SWOT factors for the Precision Gearbox Market?

Strengths: High entry barriers, strong demand from high‑value sectors, and continuous technological innovation.

Weaknesses: Costly production processes and dependence on raw‑material availability.

Opportunities: Growth in electric aviation, collaborative robotics, and medical mini‑devices.

Threats: Potential trade restrictions affecting component imports and rapid technology shifts that may render legacy designs obsolete.

How is the value chain structured in the Precision Gearbox Market?

The value chain begins with raw‑material sourcing (high‑grade steel, alloys), followed by precision machining, heat treatment, and surface coating. Next is assembly and testing, where quality assurance is critical. Distribution includes direct sales to OEMs and a network of authorized distributors. After‑sales services—maintenance, refurbishment, and technical support—complete the chain, adding value and fostering long‑term customer relationships.

What investment insights are key for stakeholders considering the Precision Gearbox Market?

Investors should target companies with strong R&D pipelines and diversified application portfolios, especially those serving aerospace and robotics. Strategic partnerships with material suppliers can mitigate raw‑material cost risks. Acquisitions of niche technology firms provide rapid entry into emerging segments such as electric aircraft gearboxes. Geographic focus on Asia‑Pacific offers volume growth, while maintaining a presence in Europe secures premium‑price contracts.

What conclusions can be drawn from the Precision Gearbox Market analysis?

The market is on a robust upward trajectory, underpinned by a 10.25 % CAGR and a projected value of $8.39 billion by 2033. Innovation, especially in lightweight and high‑efficiency designs, is a primary growth engine. Competitive dynamics favor firms that combine technical excellence with global service capabilities. Regional opportunities are strongest in Asia‑Pacific, yet demand remains solid across all major economies.

What methodology was employed to conduct this research?

The study utilizes a combination of primary interviews with industry experts, secondary data collection from company reports, trade publications, and government databases, and quantitative modeling to extrapolate future market size. Trend analysis and competitive benchmarking were applied to validate assumptions and ensure reliability of the forecast.

What is the scope of this research and its limitations?

The research covers the global Precision Gearbox Market, segmenting it by application and product type, and analyzing regional performance. It excludes detailed financial breakdowns beyond the provided market size and CAGR, and does not quantify market share percentages for individual companies or regions due to data constraints.

Which key companies have recently announced notable developments in the Precision Gearbox Market?

Recent activities include Apex Dynamics launching a new lightweight planetary gearbox for UAVs, Harmonic Drive Systems introducing a smart‑sensor‑enabled series for industrial robots, and SEW‑EURODRIVE announcing a joint venture with a semiconductor firm to integrate IoT monitoring. Nidec Corporation reported a partnership with a leading automotive supplier to develop compact gearboxes for electric drivetrains, while WITTENSTEIN SE unveiled a next‑generation right‑angle gearbox aimed at medical devices.